Building on our previous FRS 102 articles, this piece focuses on what happens at the point of transition – particularly in relation to lease accounting and revenue recognition – and what businesses need to think about when applying the revised standard for the first time.

While much of the attention has been on the ongoing accounting, the transition itself brings a number of practical and judgmental challenges.

Getting this right early will make a significant difference to how smooth the process is.

Lease accounting

Often misunderstood and/or misinterpreted, we frequently receive queries over whether the move to recognising leases on-balance sheet requires all lease arrangements to be revisited from their inception (or commencement date), including preparing the relevant calculations under the revised standard and, where required, restating comparative figures.

In short, this is not the case.

The revised standard aims to ensure transitional adjustments are applied consistently and introduces a simplified solution through its ‘modified retrospective approach’. Under this approach, lease arrangements are, somewhat counterintuitively, largely dealt with prospectively, with the restatement of comparatives not permitted.

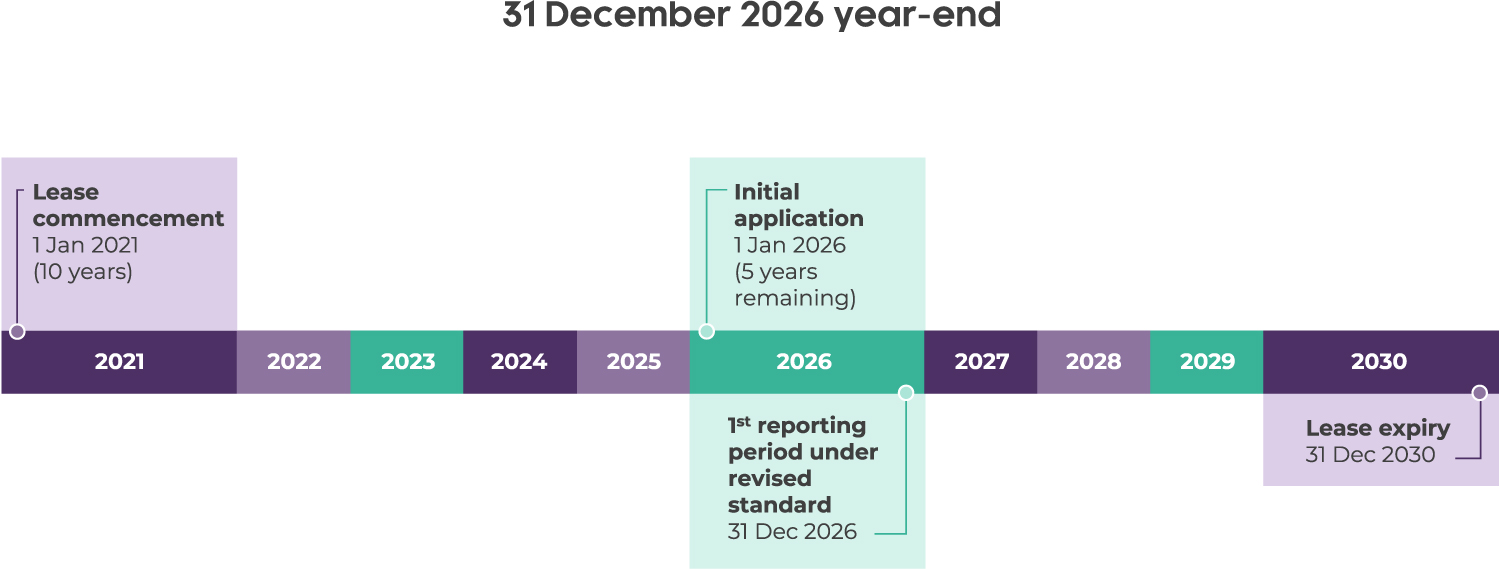

The term ‘retrospective’ instead refers to the requirement to assess existing lease arrangements under the revised standard at the date of initial application, with the cumulative effect of applying the new requirements recognised, where applicable, as an adjustment to the opening balance of retained earnings.

Once the initial date of application is determined, lease arrangements will typically fall into three categories based on their previous accounting treatment:

1. Operating leases

The date of initial application becomes the key reference point for subsequent lease calculations under the revised standard. For arrangements previously classified as operating leases, a lease liability is recognised based on the present value of the remaining lease payments at that date.

A corresponding right-of-use (‘ROU’) asset will typically be recognised at an amount equal to this initial lease liability. However, care is required where the comparative balance sheet includes lease-related balances, such as:

- prepaid or accrued lease (rental) payments

- accrued lease incentives (e.g. rent-free periods)

- impairment or onerous lease provisions

These balances are adjusted against the ROU asset and can result in a difference between the ROU asset and the lease liability initially recognised.

2. Finance leases

In contrast, arrangements previously classified as finance leases are expected to present fewer challenges, as they are already recognised on-balance sheet.

In these cases, the ROU asset and corresponding lease liability are recognised at the carrying value of the existing asset and finance lease liability immediately before the date of initial application (see diagram above). This avoids the need to establish a discount rate at transition.

However, the revised lease requirements are subsequently applied, with the lease liability measured at amortised cost using the effective interest method. This may result in some changes to the pattern of expense recognition going forward.

3. IFRS consolidation

FRS 102 preparers who report into an IFRS consolidation, and where lease accounting adjustments are prepared under IFRS 16 for group reporting, can utilise a practical expedient within the revised standard.

This allows those IFRS 16 figures to be used at the date of initial application, with any difference between the ROU asset and lease liability recognised within retained earnings (equity).

Other practical expedients / key considerations

- Exemptions are available for short-term leases (less than 12 months, including ongoing arrangements which were longer than 12 months at commencement, but where there is less than 12 months left on the lease on initial application) and low-value asset leases, with judgement required over what constitutes ‘low-value’

- There is no requirement to reassess previous contracts against the revised definition of a lease (referred to as ‘grandfathering’)

- Single discount rates can be applied across a portfolio of leases with similar characteristics (lease term, class of asset etc.)

- Hindsight can be used when assessing lease terms as a key judgement, including the actual outcomes around options to extend/terminate a lease arrangement

- Existing onerous lease provisions can be used and adjusted against the ROU asset

- There is an option to use the lessee’s ‘obtainable’ borrowing rate rather than the ‘incremental’ borrowing rate, which is expected to be simpler to determine

Disclosure requirements

There will be additional disclosure requirements across lease accounting more generally. At the point of initial application, key disclosures include:

- The adjustment to the profit and loss account in the current period (or, where impracticable, an explanation of why this is the case – although this is expected to be rare)

- The nature of the change in accounting policy (as per existing FRS 102, para 10.13)

- Practical expedients applied

- A description of the transitional provisions adopted

Revenue recognition

In contrast to lease accounting, the revised Section 23 for revenue from contracts with customers introduces an accounting policy choice on initial application:

1. Modified retrospective approach

The cumulative effect is recognised as an adjustment to opening retained earnings, with no restatement of comparatives. This is applied retrospectively only to contracts that are not complete at the date of initial application.

2. Full retrospective approach

Comparatives are fully restated, to the earliest period practicable, as if the new accounting policy had always been applied.

Other practical expedients / key considerations

- No restatement is required for contracts completed within a single reporting period, or those which were complete at the beginning of the comparative period

- Variable consideration can be calculated using the transaction price at the date the contract was completed, rather than estimating amounts for prior reporting periods

- Simplifications are available to reflect the aggregate effect of all contract modifications occurring before the beginning of the earliest period presented, or before the date of initial application, when identifying satisfied and unsatisfied performance obligations, determining the transaction price, and allocating that transaction price to those obligations.

- An exemption is available from disclosing, for prior periods presented, the quantitative or qualitative explanation of the significance of unsatisfied performance obligations, and when those obligations are expected to be satisfied.

Disclosure requirements

Disclosure requirements for the amendments to revenue recognition depend on the approach adopted on initial application. A full retrospective approach requires transitional disclosures in line with existing FRS 102 requirements for changes in accounting policy, including the amount of any adjustment for each financial statement line item (‘FSLI’) affected. Certain exemptions are available where the modified retrospective approach is used.

Practical tips

- Early preparation is key in anticipating the potential impact of initial application across lease accounting, revenue recognition and other areas of the revised standard

- An initial impact assessment should be performed over the accounts, as the commercial and technical implications can be wide-ranging (including company size, financial covenants, business valuations and distributable reserves)

- Quality disclosure checklists should be used to ensure compliance of financial statements

Other transitional considerations

Although outside the scope of this article, there are other areas to be aware of when initially applying the amendments to FRS 102, including:

- Fair value measurement

- Supplier finance arrangements

- Business combinations and goodwill

- Uncertain tax treatments

How we can help

UNW’s team includes specialists who supported clients through adoption of IFRS 15 and 16 in 2018–2019 and have experience working with businesses already applying these approaches in practice.

Whether you need impact assessments, technical guidance or practical implementation support, we can tailor our approach to your needs.

If you’d like to discuss how the new FRS 102 requirements apply to your organisation, please get in touch with your usual UNW contact or email enquiries@unw.co.uk.